When a unknown bank named as a Trustee for a securitized trust (usually Deutsche Bank, Bank of NY Mellon, US Bank National, etc.) sends you a letter stating you owe them money and you are in default, the first thing you should do is contact a local title company and have them look for an Assignment of Mortgage under your address or tax key number (it won’t likely be under your name). Chances are the Assignment of Mortgage is fabricated and void; however, this is the breeder document that allows the banksters to foreclose.

When a unknown bank named as a Trustee for a securitized trust (usually Deutsche Bank, Bank of NY Mellon, US Bank National, etc.) sends you a letter stating you owe them money and you are in default, the first thing you should do is contact a local title company and have them look for an Assignment of Mortgage under your address or tax key number (it won’t likely be under your name). Chances are the Assignment of Mortgage is fabricated and void; however, this is the breeder document that allows the banksters to foreclose.

The following information will assist you in searching the Securities and Exchange Commission (SEC) for the alleged trust.

Once you have the name of the trust and a copy of the Assignment (if any), the next move is to research the securitized trust on the Securities and Exchange Commission (SEC) website. Here is an example of an Assignment of Mortgage with Deutsche Bank National Trust Company, as Trustee of the IndyMac INDX Mortgage Trust 2007-FLX3, Mortgage Pass-Through Series 2007-FLX3 under the Pooling and Servicing Agreement Dated April 1, 2007. This assignment was made 3 years after the trust closed.

The easiest way to find the trust is to open the SEC website – Click HERE to open the SEC website [www.sec.gov]; and go to the top right-hand side of the SEC header and Click “More Search Options”.

You’ll find a light blue search box. (1) Click the “● Contains” button and (2) enter the year and trust code, for example: 2007-FLX3; (3) Click the “Find Companies” at the bottom of the blue box. Click HERE to reach the “Search Options” page.

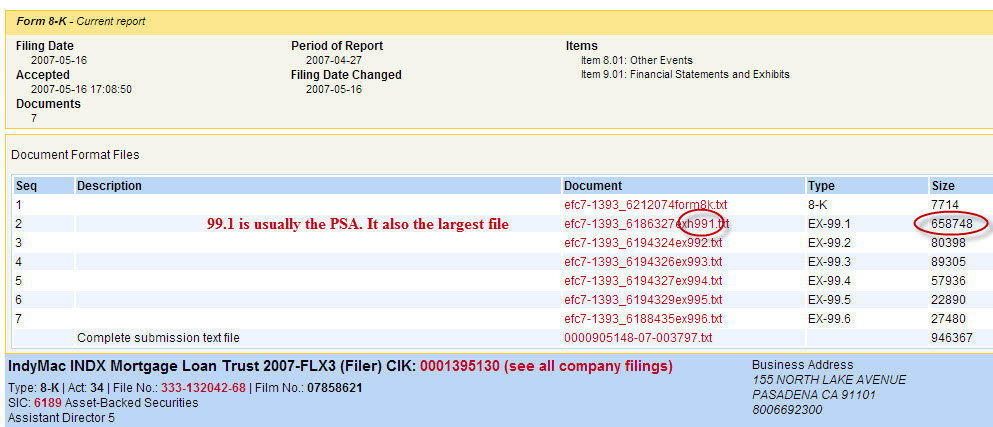

Sometimes it will give you a list of Trusts (identified by 6189 code) to choose from and you will match the rest of the information on the Assignment or Letter from the Trustee to that specific Trust. In this instant – the year and the trust code will take you right to the securitized trust – IndyMac INDX Mortgage Trust 2007-FLX3. Below is the picture of the SEC master file for this trust – Click HERE for the SEC Master Trust File.

The entire Trust is worth reading and will give you a better picture of the securitization scheme. You will note hundreds of warning to investors that these trusts are really risky. Starting from the bottom the FWP is an acronym for FREE WRITING PROSPECTUS SUPPLEMENT. In some trusts you will find what they call a “loan tape” where alleged loans are listed, not by name, but by identifiers. In this example, the loan tape is in the FWP as noted above – Click HERE for the loan tape example.

The Pooling and Servicing Agreement (PSA) is sometimes found under the FWPs and in this case it is under the 8K. An easy way to spot the PSA is by the size of the file. It is usually the largest file in the group and that’s a good place to start. Click HERE for the PSA example.

The PSA will provide you with pertinent information as it is the controlling document of the trust. Article One will give you the Definitions. If you have a “Find” control on your computer it makes it easier to search for the Closing Date, the Cut-Off Date, the Governing Law and the Conveyance of Mortgage Loans, which is traditionally located under Article II, 2.01.

Read Article Two Conveyance of Mortgage Loans very carefully. It will tell you how and when the mortgage loans were to have sold, assigned, and transferred to the trust. If the trust is governed under New York law, “Under New York Trust Law, every sale, conveyance or other act of the trust on contravention of the trust is void. EPTL §7-2.4. Therefore, the acceptance of the note and mortgage by the trustee after the date the trust closed, would be void.” See Wells Fargo Bank, N.A. v. Erobobo, 042913 NYMISC, 2013-50675.

ORDER CERTIFIED COPIES OF THE TRUST DOCUMENTS FROM THE SEC

ORDER CERTIFIED COPIES OF THE TRUST DOCUMENTS FROM THE SEC

Now, after you have located your trust – you can order a “certified” copy from the SEC. It will come with blue ribbons and a gold seal – all dressed up for the Judge.

Click HERE for the Request for Certification and refer to your specific SEC Master Trust File. You can request all of the documents in the trust and the SEC will send you a bill with the documents (make sure you pay it immediately) – even to Hawaii the entire certified trust documents cost $32.

You will primarily want the PSA and the Prospectus.

You are going to order by the FILE/FILM NUMBER. When you order – put the red number / and the black one underneath.

One more thought to consider –

WHISTLEBLOWER

Blow the Whistle if your assignment was made after the Closing Date of the trust. You can file a form and upload your fabricated Assignment of Mortgage.

A whistleblower who knows of possible securities law violations can be among the most powerful weapons in the law enforcement arsenal of the Securities and Exchange Commission. Through their knowledge of the circumstances and individuals involved, whistleblowers can help the Commission identify possible fraud and other violations much earlier than might otherwise have been possible. That allows the Commission to minimize the harm to investors, better preserve the integrity of the United States’ capital markets, and more swiftly hold accountable those responsible for unlawful conduct.

The Commission is authorized by Congress to provide monetary awards to eligible individuals who come forward with high-quality original information that leads to a Commission enforcement action in which over $1,000,000 in sanctions is ordered. The range for awards is between 10% and 30% of the money collected. To file a whistleblower form and upload your fabricated Assignment of Mortgage – Click HERE.

The Commission is authorized by Congress to provide monetary awards to eligible individuals who come forward with high-quality original information that leads to a Commission enforcement action in which over $1,000,000 in sanctions is ordered. The range for awards is between 10% and 30% of the money collected. To file a whistleblower form and upload your fabricated Assignment of Mortgage – Click HERE.

Maybe if we all start uploading our fabricated, bogus, fraudulent Assignments of Mortgage by the hundreds – the government will begin to get a better picture of the fraud.

Good luck to all.

![]()

This is a really excellent information for everyone who has a mortgage, Mahalo

A bogus assignment ALSO voids the REMIC status of the trust meaning the trust then owes potentially millions of dollars in tax money! I reported my trust in 2010 to the IRS as a whistleblower and even though the IRS will go after an individual they have thus far failed to go after the trusts. If we (common folk) know what is happening then how could the politicians not know?

Not exactly true…there has never been any acceptance of the assignment by the trustee for the trust. It is solely the sub-servicer filing the assignment to foreclose.

New York is one of two states where an ultra vires transfer of assets to or by a trustee on behalf of a trust is void rather than voidable. If the transfer were voidable then the damaged party would have to bring an action against the misfeasing parties to have the transfer voided. In New York the transaction is void ab initio, just like it never happened.

You can read more here: http://foreclosuredefenseschool.com/erobobo-eptl-7-2-4-widows-and-orphans/

Can ups say this in Layman’s terms please. Also, it seems we are in an illegal mortgage that was a banned in 2002 but we were put into it by Country Wide in 2006 and despite a loan modification in 2008 that we complied with for 5 years, we ended up back in this illegally banned loan and remain there. 5 years and 12 attempts at a new loan modification and the bank again tried to put us into an illegally banned loan.

The whole modification thing is a scam. Many have had their homes taken away even though they were always paying on time. Part of the agreement is to be able to take away your home in foreclosure and you can’t fight it. From what I read, buyers are given lower payment schedule and then eventually, they are going to increase the payments and the homeowner ends up not being able to pay off house again. May God bring these banksters to justice.

HMMM!!! So in 2006, we are put into a loan that I did not know had been banned in 2002. We noticed that it was negatively amortizing because we could not afford any of the other 3 option arms on it. This is illegal in CT but as I said, we did not know this. We had never ever missed a payment or been late but needed a loan modification because of it negatively amortizing. October 2008, we sign a 5 year loan modification with Country Wide even though June 2008, Bank of America has take over. 2010, I become legally disabled on SSDI/SSI. I contact them asking them to convert our then loan modification to a permanent loan as my debt to income ratio will not match our loan payments when the loan modification ends. They refuse and we end up back in the banned illegal loan and spend the next 5 years plus making 12 applications for loan modifications. The point is that when I became disabled, under FEDERAL ADA law (American Disability Act) Title I, Title II, Title III, Title IV, Title V etc., if I make a reasonable accommodation or modification request, they must honor it or provide me with an alternative that is reasonable. They did not. Additionally, after our 12 attempt at a modification, they gave us a new loan mod but would to tell us the terms after we did the 3 month trial. At the end of the 3 months, they again tried to put us into an illegal loan which contained balloon payments. So between the illegal loans, the ADA violations, and we think they may have lost the paperwork, we ware wondering were we actually stand. Especially as it is now gong on 6 years with no attempts at foreclosure.

Common misunderstanding of REMIC (Real Estate Mortgage Investment Conduit) trusts. The Name of the Trust is the name of the Depositor who also did all the filings with the SEC. The Depositor is a special purpose entity (normally owned by the Trust Sponsor who bought the notes from the original lender) and is the last legal owner of the notes/mortgages and is necessary under trust law to make the note assets bankruptcy remote. As most Depositors created more than one trust, CWALT — for example — created many hundreds of them, There is also a 4 number/letter designation that identifies the particular trust together with the year the trust closed. No trust exists until it is closed. The Depositor has nothing more to do with the trust (a special purpose vehicle) once the notes are deposited. The Trustee issues the security certificates back to the Depositor who together with an underwriter sold them to investors. Every REMIC trust also has a Master Servicer. Both the Trustee and Master Servicers in many REMIC trusts have undergone changes due to bank mergers, etc. Mortgage assignments that say the trustee paid consideration for the note are pure bullshit as the trustee pays for nothing in any real estate trust. it is only done that way to make it appear to be a contract when in truth there is no consideration and no acceptance.

So then if Bank of America bailed out Country Wide and CWALT is still listed as the private investor according to the servicer, what does that mean? As well, what does it mean if they put me into and left me in a loan in 2006 that was banned 4 years earlier in 2002?

Excellent information, Banks and mortgage companies steal homeowners property by Assignment of mortgage

All mortgage assignments are bogus. They are made to look like contracts, but they are not as there is never any consideration or acceptance. No trustee ever accepts a mortgage assignment. The mortgage assignment is ONLY used to prove standing, i.e. that the holder is suing after they owned the note. They are also created by servicers who normally are not parties to the trust and have no standing of their own. They claimed to be an “Attorney in fact” which is a way of claiming they have a Power of Attorney, but they seldom do. Many assignments are actually in the name of the original lender which no longer exists and cannot have any agents or issue a PofA. The fundamental reason that mortgage assignments are even needed is because the Notes were never endorsed into the trusts as the PSA required. Also, endorsements are usually not dated and are in blank, thus a Mortgage Assignment is needed to establish standing. The main way to destroy a mortgage assignment is if it does not also assign the Note. Then it accomplishes nothing and is not admissible.

So here is an interesting one. January 2008, Bank of America is asked to bailout CountryWide. June 2008 it is official that BANA (Bank of America) now owns Countrywide. October 2008, BANA has us sign a loan modification with CountryWide letterhead and what I would think are countrywide employees. HMMM! This would make this document illegal I would think. Thoughts? This is after we were put into a illegal loan in 2006 that had been banned in the state of CT in 2002.

My loan is owned by Fannie Mae. How can those of us whose loan is claimed by a GSE find our PSA, Our loans are definitely securitized as MERS is the beneficiary. How does one find Fannie Mae’s Trust.

Not exactly. The Government Sponsored Enterprises (Freddie, Fannie, and Ginnie) don’t use the same instruments as private label issuers do nor are they required to file with the SEC. That said, you can get information if you know where to look and have a little something to go on. For instance Freddie’s equivalent of a PSA (called a PC Trust Agreement) can be found on there site at: http://www.freddiemac.com/mbs/html/legal_doc.html

They reuse these “master” documents for each issuance until it is replaced by a newer model so if your loan went to Freddie in, say, 2007 you have to go some where else on the site (http://www.freddiemac.com/mbs/html/hislegal_doc.html) because ” Freddie Mac adopted trust agreements for its mortgage securities on December 31, 2007.”

In the historical section you will find links to “Mortgage Participation Certificates Agreement” which was the pre-2008 version of the newer PC Trust Agreement. In the case of a loan going in to a trust on January 2007 you would refer to the October 14, 2005 (not the March 19, 2007) agreement to find the terms.

If you can get the Committee on Uniform Securities Identification Procedures (CUSIP) number or pool number for the pool your loan went into you can get more detailed information at: http://www.freddiemac.com/mbs/html/sd_pc_lookup.html?intcmp=SMSSL-T

Fannie and Ginnie have similar information on their sites it just takes some digging.

check with your local county recorders office and see if there has already been an assignment done to the trust. This makes it much easier to locate.

Assignments are not usually filed until there is an alleged default. Also, the assignment is NOT filed under the homeowner’s name. It is usually found under the address or tax key number and associated with the mortgage. A title company can assist with an assignment search.

But just because there is an assignment DOES NOT MEAN that the loan is not in a trust. I have found several loan numbers actively trading in trusts that appeared to have been assigned to the servicer. Never assume the loan is not securitized until you have a professional search of the loan number.

This post was prepared for those folks who know the name of the alleged trust. As we all know now by the PHOENIX LIGHT, et al v JPMORGAN CHASE & CO, et al lawsuit – nothing was assigned… Congress has already advised homeowners that the banks “don’t have the paper” and the 2010 SENATE COP report laid out the facts that loans were not in the trusts and the REMICs were empty. It’s just the judiciary not listening en masse – just the intelligent judges have figured it out. The rest are trying to protect their pension funds and stock portfolios.

This assignment fraud is what the FDIC has covered up in IndyMac and Wamu: https://deadlyclear.wordpress.com/2013/06/02/fdic-hide-sneak-and-seal/. More to come…

How do you determine if the trust is governed by NY Securities Law?

When you find the trust on the SEC – go to the PSA and search for the Governing Law section (usually about sec 10, 11 or 12). It will read like this:

Section 12.03 Governing Law. THIS AGREEMENT SHALL BE CONSTRUED IN ACCORDANCE WITH AND GOVERNED BY THE SUBSTANTIVE LAWS OF THE STATE OF NEW YORK APPLICABLE TO AGREEMENTS MADE AND TO BE PERFORMED IN THE STATE OF NEW YORK AND THE OBLIGATIONS, RIGHTS AND REMEDIES OF THE PARTIES HERETO AND THE CERTIFICATEHOLDERS SHALL BE DETERMINED IN ACCORDANCE WITH SUCH LAWS.

First of all, thanks for getting back with me so quickly. Greatly appreciated.

I have gone through the prospectus and PSA with a fine tooth comb and cannot find the governing law. I am researching cwalt 2004-36cb and believe me, that language isn’t in there. Sigh

The full name of the trust in question is CWALT INC – ALTERNATIVE LOAN TRUST 2004-36CB. It’s always helpful to have all the information. The Central Index Key (CIK) is 0001313080; think of it like the SSN for the company on Electronic Data-Gathering, Analysis, and Retrieval (EDGAR) system. In any even the PSA for the trust in question states:

SECTION 10.03. Governing Law.

THIS AGREEMENT SHALL BE CONSTRUED IN ACCORDANCE WITH AND GOVERNED BY THE SUBSTANTIVE LAWS OF THE STATE OF NEW YORK APPLICABLE TO AGREEMENTS MADE AND TO BE PERFORMED IN THE STATE OF NEW YORK AND THE OBLIGATIONS, RIGHTS AND REMEDIES OF THE PARTIES HERETO AND THE CERTIFICATEHOLDERS SHALL BE DETERMINED IN ACCORDANCE WITH SUCH LAWS.

Aloha, It’s a pretty good tutorial.

Michael

Pingback: Follow the Money Trail | Freedom Truth

THE USURERS OF DEUTSCHE BANK ARE RULING IN GREECE WITH SLAVERY, ROBBERY AND GENOCIDES

1} THE GREEK POLICY IS COMPLETELY CONTROLLED BY DEUTSCHE BANK THROUGH ITS PUPPETS samaras AND venizelos.

https://en.wikipedia.org/wiki/Antonis_Samaras https://en.wikipedia.org/wiki/Evangelos_Venizelos

“Deutsche Bank writes German Finance Ministry’s Greek debt policy, ARD documentary reveals

The German government’s policy on debt restructuring for Greece is lifted directly from policy papers prepared by the Deutsche Bank, it has emerged.

The proposal floated at the beginning of June by the German Finance Minister Wolfgang Schäuble for a voluntary bond swap leading to a prolongation of the outstanding Greek sovereign bonds by seven years is based on a document by Deutsche Bank, investigative reporters from Germany’s ARD TV station have revealed.

http://www.wdr.de/tv/monitor/sendungen/2011/0616/Griechenland.php5

The Deutsche Bank document called “Proposal for Greek liability management exercise – burden sharing without haircuts” insisted, not surprisingly, on a voluntary participation by banks.

The revelation that the Finance Ministry in Berlin just takes over the contents of policy papers of Deutsche Bank offers yet more proof that Chancellor Angela Merkel and Wolfgang Schäuble are puppets of the commercial banks.

Merkel and Deutsche Bank CEO Josef Ackermann attended this year’s Bilderberg conference in Switzerland and would have had ample opportunity to discuss ways and means to expropriate yet more money from the tax payers under one pretext or another. ”

http://www.corpwatch.org/article.php?id=15732

2) DEUTSCHE BANK DEPRIVES THE GREEK PEOPLE OF THE MEDICAL INSURANCE

” Recently Greece took the «honor» of first place in Europe for reducing budget expenditures on health services. In particular, expenditures on medications were reduced from 5.6 billion euros (2010) to 3.8 billion euros in 2011 and to 2.88 billion euros in 2012. As a direct result of this, over 50 world pharmaceutical companies have discontinued shipments of medications to Greece. It has become common for relatives of hospital patients to have to run exhausting marathons from pharmacy to pharmacy in search of needed medications. There is an acute shortage of medical equipment. State hospitals are short around 6,500 doctors and 20,000 nurses and orderlies; massive numbers of medical professionals are leaving the country.

Even those who are employed have difficulty paying for medical services, whose prices have abruptly shot up. More and more often people don’t have the money to obtain quality medical assistance, especially in rural regions and on the islands. In a UN expert report published in May 2013, it was noted that over 10% of the total population of the country live in conditions of extreme poverty. Greece remains the only country in the Eurozone with no complex social assistance scheme, healthcare services are almost inaccessible to poor and low-income citizens, and almost a third of the population does not have state medical insurance. ”

http://www.strategic-culture.org/news/2013/08/18/greece-a-social-explosion-is-inevitable.html http://www.keeptalkinggreece.com/2013/07/30/athens-sos-urgent-appeal-for-cancer-patient-without-insurance

3) GREECE IS ONE OF THE FEW STATES OF THE WORLD THAT KEEPS THE PRISON FOR DEBT AND THE UNIQUE IN EUROPE.

” Debts and Prison Penalties

A debtor owing

5,000 euro may go to prison to 12 months

10,000+ euro – at least 6 months

50,000+ euro – at least one year

150,000+ euro – at least three years ”

4) DEUTSCHE BANK BLACKMAILS AND CUTS THE ELECTRICITY IF GREEKS DO NOT PAY EXORBITANT TAXES ON THE PROPERTY.

http://www.guardian.co.uk/business/2011/sep/27/greece-property-tax-vote-venizelos

http://histologion.blogspot.gr/2013/02/the-greek-debacle-2013-of-paupers-and.html

5) GREECE IN CRISIS-DRAMATIC INCREASE OF SUICIDES: 3,124 PEOPLE IN 2009-2012

6) ATHENS: DEAF-MUTE WOMAN THREATENING TO COMMIT SUICIDE RESCUED

” The president of Deaf Federation told reporters that the woman is not the only one in desperate situation because her social welfare allowances have been cut.

“All deaf people in this country are in the same situation because they have not received their welfare allowances for the last 6-8 months.”

Greece saw a sharp increase of suicides due to economic problems after the country sought the aid of the International Monetary Fund.

According to Greek Police from May 2010 until now, 837 suicides have taken place. Greek police answered a relevant question on the number of suicides posed by several MPs at the Parliament.” http://www.keeptalkinggreece.com/2012/12/18/athens-deaf-mute-woman-threatening-to-commit-suicide-rescued/

WHO CONTROLS DEUTSCHE BANK ?

WE CAN NOTICE RELATIONS AMONG LORD JACOB ROTHSCHILD AND DEUTSCHE BANK.

DAVID HAYSEY ” HEAD OF PUBLIC EQUITIES AT RIT CAPITAL PARTNERS ” AND IN THE PAST ” DIRECTOR AT J ROTHSCHILD CAPITAL MANAGEMENT ” HAS BEEN ” MANAGING DIRECTOR AT DEUTSCHE BANK ” http://uk.linkedin.com/pub/david-haysey/1b/470/bb3

” In 2012 RIT Capital saw management changes with the exit of investment director Mikael Breuer-Weil and the appointment of Ron Tabbouche. The first half of 2013 saw further changes with the resignation of David Haysey, head of public equity and manager of the RIT global quality portfolio. ” http://www.iii.co.uk/articles/110881/oriel-rates-lord-rothschilds-rit-capital-positive

RON TABBOUCHE HAS BEEN SALES ANALYST AT DEUTSCHE BANK. http://www.trustnet.com/Managers/ManagerFactsheet.aspx?personCode=00000065RA&univ=O

Today, Jacob [Rothschild] is Chairman of RIT Capital Partners plc, one of the largest investment trusts quoted on the London Stock Exchange with a net asset value of about £2 billion.[5] He is Chairman of J Rothschild Capital Management, a subsidiary of RIT Capital Partners plc. https://en.wikipedia.org/wiki/Jacob_Rothschild,_4th_Baron_Rothschild

THERE ARE ALSO LINKS AMONG EVELYN DE ROTHSCHILD AND DEUTSCHE BANK.

VERNON JORDAN, THE BIG FRIEND OF EVELYN DE ROTHSCHILD AND LYNN DE ROTHSCHILD, HAS BEEN A DIRECTOR OF DEUTSCHE BANK.

http://www.companiesintheuk.co.uk/director/8570529/vernon-jordan-jr

” LYNN [the wife of EVELYN DE ROTHSCHILD] is the CEO of ELR Holdings and became a director of The Economist in 2002. She launched FirstMark Communications in the late 1990s and got EVELYN DE ROTHSCHILD, Henry Kissinger, Vernon Jordan (senior managing director LAZARD; close Clinton friend and advisor; friend of EVELYN DE ROTHSCHILD; permanent Bilderberg visitor), Michael J. Price (former managing director LAZARD), Nathan Myhrvold (former CEO Microsoft; PPI Task Force member), and others as its initial directors.”

” In late August 2004, Clinton and his wife Hillary, EVELYN DE ROTHSCHILD, LYNN DE ROTHSCHILD, Vernon Jordan, and Prince Andrew were all hanging out at the Vineyard at their very own “Anyone but Bush” party. Rothschild and Jordan were jointly celebrating their birthdays that day. Together with his wife he attended the 32nd Williamsburg Conference in Delhi in 2004. ” https://wikispooks.com/ISGP/organisations/introduction/PEHI_Evelyn_de_Rothschild_bio.htm

DEUTSCHE BANK IS CONNECTED ALSO WITH THE EDMOND DE ROTHSCHILD OWNED BY BENJAMIN DE ROTHSCHILD. https://en.wikipedia.org/wiki/Benjamin_de_Rothschild

http://hk.linkedin.com/pub/jeffrey-yu/1a/347/18b http://www.linkedin.com/pub/florence-dodard/31/679/566 http://it.linkedin.com/pub/elena-giordano/5/589/7a1 http://www.linkedin.com/pub/lorenzo-avico/6/346/238

” Deutsche Bank, now the number one derivatives- and currency-trading bank in the world through its City of London operation, survived to become what it is now — a monster with a $72 trillion derivatives portfolio — because it was massively bailed out in October 2008 by Timothy Geithner and the New York Fed.” http://larouchepac.com/node/26698

DEUTSCHE BANK MASSACRES SICK AND DISABLED PEOPLE IN UNITED KINGDOM

1) UNITED KINGDOM IS A PROTECTORATE OF DEUTSCHE BANK

http://blogs.telegraph.co.uk/news/maryriddell/100033519/with-bankers-as-his-friends-david-cameron-needs-no-enemies/

2) DAVID CAMERON’S FAMILY FORTUNE : THE JERSEY, PANAMA AND GENEVA CONNECTION

http://www.guardian.co.uk/politics/2012/apr/20/david-cameron-jersey-panama-geneva

http://www.mirror.co.uk/news/uk-news/conservative-party-links-to-fat-cat-103271

http://www.independent.co.uk/news/uk/politics/163850bn-official-cost-of-the-bank-bailout-1833830.html

3) MAN WHO CAN’T TALK, WALK, OR FEED HIMSELF HAS HIS BENEFITS STOPPED AND IS TOLD TO PROVE HE’S UNABLE TO WORK

http://www.dailymail.co.uk/news/article-2420711/Benefits-stopped-Darlington-man-talk-walk-feed-prove-work.html

4) ATOS BENEFITS BULLIES KILLED MY SICK DAD, SAYS DEVASTATED KIERAN, 13

http://www.dailyrecord.co.uk/news/scottish-news/atos-killed-my-dad-says-boy-1411100

5) RETIRED BLIND MAN IS ‘FIT FOR WORK’

http://www.burytimes.co.uk/news/10701849.Retired_blind_man_is__fit_for_work_/

6) AROUND 4,400 PEOPLE COMMIT SUICIDE IN ENGLAND EACH YEAR – THAT’S ONE DEATH EVERY TWO HOURS – AND AT LEAST 10 TIMES THAT NUMBER ATTEMPT SUICIDE

http://www.mentalhealth.org.uk/help-information/mental-health-a-z/S/suicide/

7) MAN WITH TERMINAL BRAIN CANCER TOLD HE’S ‘FIT FOR WORK’

“A man with terminal brain cancer is among those being told they are ‘fit for work’ under the government’s work capability assessment programme, new research has discovered.

Other figures told they would lose their disability benefit included someone with no short-term memory mechanism and an incontinent disabled man who is both blind and deaf.” http://politics.co.uk/news/2012/11/12/man-with-terminal-brain-cancer-told-he-s-fit-for-work

8) DEUTSCHE BANK ABOLISHES THE POSSIBILITY OF SICK AND DISABLED PEOPLE TO APPEAL THE DECISIONS THAT CUT THEIR BENEFITS CONDEMNING THEM TO DEATH http://blacktrianglecampaign.org/2013/08/29/draft-deregulation-bill-government-moves-to-shut-down-judicial-supervision-and-criticism-of-dwp-atos-decision-making-by-abolition-of-duty-by-tribunals-president-to-publish-annual-report/

9) BRITISH GOVERNMENT APPOINTS PRIVATE INSURANCE COMPANY UNUM IN ORDER TO DESTROY WELFARE SYSTEM

10) OVER 70 MPs CONNECTED TO COMPANIES INVOLVED IN PRIVATE HEALTHCARE

http://socialinvestigations.blogspot.co.uk/2012/07/over-60-mps-connected-to-companies.html

11) OVER 200 PARLIAMENTARIANS HAVE RECENT PAST OR PRESENT FINANCIAL LINKS TO COMPANIES INVOLVED IN HEALTHCARE

http://socialinvestigations.blogspot.co.uk/2012/02/nhs-privatisation-compilation-of.html

12) UNITED KINGDOM GOVERNMENT DENOUNCED FOR CRIMES AGAINST DISABLED PEOPLE TO INTERNATIONAL CRIMINAL COURT IN THE HAGUE

https://217.72.179.33/members/www.bilderberg.org/phpBB2/viewtopic.php?t=5076

What if your loan is in an unregistered Securitization trust.. It says on my assignment Stanwich Mortgage Loan Trust Series 2012-17. I searched and cannot find it.

Looks like it was registered. The SEC lists it anyway. Go down to the 6th record. http://www.sec.gov/Archives/edgar/data/1541924/000114420413046166/v353001_ex99-1.htm

I have a friend a Title Company that just pulled a report and it does not show any Assignment of Mortgage having ever been recorded, although I know that my loan has been sold at least three times. The Notice of Default only lists an attorneys office as substitute trustee for MERS, designated beneficiary of my original lender, now defunct. Any words of advice on how to proceed? I went onto MERSId and it still lists the older servicer and the new lender as JP Morgan Chase NA.

The reason there is no list of assignments is because of MERS. All the assignments went through MERS’ private system. It’s not going to be listed in anywhere outside of the MERS database. I bet your original trustee isn’t aware of any assignments too.

Sounds like you’re in foreclosure, so you have to come up with an affirmative defense to stop these clowns. Fraud is a great start. And it will work in any state. Judicial or non-judicial. You can claim breach of contract, theft or illegal mortgage too.

You should look up fraud cases in your state to find out what must be alleged in your state. If you can’t do that, then this is what must be alleged in Washington State where I live, and will probably work in every state since our state is really anal and other states usually require less elements to be proven. Even if you can’t prove fraud, you will buy more time in your house. But if you demand enough documents, like the chain of legal assignments to the lawyer, you can win that way. If they can’t show they have the right to foreclose, tell them to pound the pavement and get lost.

The 9 Elements of Fraud:

“The nine elements of fraud are: (1) representation of an existing fact, (2) materiality of the representation, (3) falsity of the representation, (4) the speaker’s knowledge of its falsity, (5) intent of the speaker that it should be acted upon by the plaintiff, (6) plaintiff’s ignorance of its falsity, (7) plaintiff’s reliance on the truth of the representation, (8) plaintiff’s right to rely upon it, and (9) resulting damages suffered by the plaintiff.” Wear v. Sierra Pacific Mortgage Company, Inc. citing: Stiley v. Block, 130 Wn.2d 486, 505 (1996).

So what that says is, 1) you have to show they presented something like a paper that was supposed to represent facts. 2) That the representation wasn’t verbal and can hopefully be brought into the court room. 3) That the representation was false. 4) That the person who made the representation knew it was false. 5) basically this means they intended for you to act on the false information. 6) That you didn’t know it was false. 7) That you relied on it being true. Make sure to say something like no reasonable person would have assumed otherwise. 8) That you had the right to rely on the information since it involved your home. 9) Then tell how it damaged you. They stole all your monthly payments when they didn’t have the right to.

And by the way, it doesn’t have to be false representations. It can be misleading or was omitted.

But that’s how you at least delay if not stop these crooks. And make MERS prove who they were representing. Who were they acting as an agent for. Make them present the paperwork showing who their principle was. An agent has to have a principle governing their actions. Otherwise they are acting as an principle which your deed doesn’t allow.

And since your mortgage was securitized, none of these crooks are a legal beneficiary under Washington State law and have the right to demand payment or to foreclose. To see a simple explanation of it all go to this page and look at the diagram I made showing what happened. (Scroll down to the bottom) http://golfegg.wix.com/pretender-lenders#!services/c1iwz you can go to this page for a better explanation. http://golfegg.wix.com/pretender-lenders#!team/galleryPage

Good luck!

Forgot to mention, get the Pooling and Service Agreement and make them prove they followed that too. Scroll down to the next comment to see how to do that.

I just wanted to let you know the easiest way to find all the documents for your mortgage, including the pooling and servicing agreement. I spent days and days looking for them and never did find them until I did this little 2 step process.

1. Call your servicer and ask who the note Holder is. They have to tell you by law.

2. Call (202) 551-7230 (SEC number) and tell them the Trust name and asked for all the certified documents for that trust. It cost me $56 for everything. (in 2015) It will take a few days, but they will send you all the documents by email in PDF format. And actually you don’t have to pay since they send them by email BEFORE you pay anything.

3. DONE! You have your certified documents from the SEC that can be used in any court.

Great information. Thank you. Is the note Holder the name of the Trust? If Fannie Mae claims to be the owner of the loan is that the same as the note Holder?

Yes I think they are claiming or implying they are the Note Holder since they are claiming to be the owner of the loan. And you got the loan by way of the Note, so that’s kind of reasonable. I wouldn’t try to attack that point, you have bigger fish to fry. And the note holder is not the name of the trust. The note holder is usually some business entity like Bank of New York Mellon. The trust name is what ever the depositor, or who ever is putting the mortgages into the trust wants to call it.

I’ve learn there are two rights to a Note that are passed on under the UCC. There is ownership rights (the owner of the note) and enforcement rights (who can enforce payment/foreclose) in a Note. The rights can be held by two different entities, but it’s best to be both. For instance, BOA could just enforce the Note, while Wells Fargo could only receive the payments/profits. Or BOA could have both rights if they’re smart. Ownership rights are determined by Article 9 of the UCC, and enforcement rights are determined by Article 3 of the UCC.

But if you’re in foreclosure, you want to stop the enforcer who is coming after you, if there is one. It doesn’t matter who receives the profit. So you should learn Article 3 of the UCC inside and out, if possible. Those are the laws that will stop them in their tracks if they screwed up the securitization process, which apparently most did.

To learn those laws, there are a few good resources online you can trust and rely on, which are written by lawyers, law professors, the American Bar Association (ABA) and the UCC Permanent Editorial Board.

A good book written by a lawyer is called “Fighting the Foreclosure Machine” which I think this site sells.

This is an easy to read powerpoint presentation done by a law professor/ABA showing the laws in Article 3 & 9 and how they relate to securitized trusts. http://tinyurl.com/js4vnsu

Here’s another good one called “What We Have Learned from the Mortgage Crisis about Transferring Mortgage Loans” by a Missouri law professor. http://tinyurl.com/z32jmfk

And I like “Dirt Lawyers and Dirty REMICs” by the ABA. http://tinyurl.com/hc6bb73

Adam Levitin wrote a lot of good articles too. (another law professor) One is called “Robo-Signing, Chain of Title, Loss Mitigation and Other Issues in Mortgage Servicing”. http://tinyurl.com/j59q3kh

Base your case on standing, real party in interest, lack of agency authority, invalid assignments or transfer of Notes or mortgages. Those are the big ones they violate most often, can bring them down and have the most success. You can get lost with all the info out there on everything these crooks did wrong.

And remember, you won’t be able to enforce the PSA unless you can prove you were a party to it by claiming it was a step transaction. Or that you are some kind of Third-party beneficiary, like a Donee, Incidental or Intended Beneficiary. Personally I think we were both and deceptively or unwittingly involved in a step transaction we were never informed of, and we are a third party beneficiary, since they couldn’t foreclose on us without it, and we received financing under it, and borrowers are mentioned in it, just like the investors were.

If you can’t prove one of those things, the crooks still need to have standing. A foreclosure requires properly pleading and proving that. (and in every other case in every court) And in order for them to have standing, they had better have done what the PSA says they were supposed to do, which most didn’t. If the trustee for the securitized trust didn’t dot every i and cross every t for your mortgage, then your mortgage didn’t make it into the trust and they have no standing to foreclose, because NY Trust Law 7-2.4 says: “every act of the trustee in contravention of the trust is void.”

So when who ever is coming after you says you can’t enforce the PSA because you’re a 3rd party to it, you can tell the court and that crook “I’m not trying to enforce the PSA, I’m challenging the standing of the Plaintiff (which the courts always allow) and the only way the Plaintiff can have standing is if they followed the PSA. If they didn’t follow the PSA, everything they did with my Note is voidable or void under the laws governing the Trust. If they didn’t follow the PSA, they aren’t a party in interest to this case, don’t own my Note, can’t enforce it, have no standing and can’t be damaged. I don’t believe they did follow it, and until they prove they did, I am not behind or late on any payments, and not in default to the one and only Note Holder who can enforce my Note under Article 3 of the UCC.”

Just keep your case simple but, Deadly Clear. Pun intended. 🙂 You’re only goal is to shoot down the current attacker as quick and efficiently as possible.

Hope that helps! 🙂

NO, see my message above. The name of the trust is the name of the Depositor who created the trust and this has absolutely nothing to do with the trustee.

THE CERTIFICATEHOLDERS IS LXS-2006-4N and not appear anymore just LXS-2006-7 instead.

Can be a change in th company names just like that ?

I have an LXS as well, and after searching, they appear to have been unregistered due to their only being a few investors. But it actually made my head hurt just to figure that out. It seems like all of the LXS series went that way, from 2007 on.

I’m going to try calling and see if I can get the pdf emailed.

What if there were additional assignments that seem to not be appearing on my land records. As well, what is the one Assignment has no end date?

I’m trying to fight a wrongful foreclosure case pro se, and I’ve been denied discovery several times. My trial date is on the 8th of March, and thy say that they are going to produce a copy of the Pooling and Servicing Agreement now, even though they refused under the request for discovery. GinnieMae was on the Assignment, at least according to the numbers shown on the document, which are as follows: GNMA Loan # 0102592392. I looked for any trust info on the document, but I can’t find anything. How do I search for the trust info, soecifically?

Thanks in advance!

Reblogged this on sandrakblog.

I own and have in my possession the Original Warrantee Deed. If my property has changed bank hands and the title turned over to others by the original mortgage company, does that mean that my Deed is no longer valid or does it mean that the title is now clouded?

ive watched recorts change I also have the deed with the vol. and book but that doesn’t matter

sandrashultz805, what does “I’ve watched records change. I also have the deed with the vol. and book but that doesn’t matter’? mean in response to my comment?

Also, the state of CT placed a bogus lien on my property, without any authenticity of it’s placement being valid, stating I got cash assistance back in 1995-1998. I know I did NOT get cash assistance and if I did, it was not for the amount on the “reconstructed” spreadsheet that they are using as their only piece of evidence. Yes, the state admitted that the spreadsheet was reconstructed but they do not know by who, what, where, when or with what. I did a Freedom Of Information Act Request for my Department of Social Services files back to 1995, it took 8 months to respond that the files are either lost of destroyed.I tried to fight it but I could not afford an attorney and was not allowed to present my case. Yet, they refuse to remove the lien and the judges refused to remove it. Long story shortened, the lien has NO Dollar amount on it and says, for past, present and future cash assistance. Not only did I not get cash assistance, and the state cannot prove that I did, but I do not get cash assistance in the present, and it would seem to be illegal for someone to lien something that has not happened in the future. This lien clouds my title/deed and my house is underwater, so wondering if anyone knows proper law on State Liens and the placing of any liens for that matter.

sandrashultz, I am unsure of what your response means, ie. ive watched recorts change I also have the deed with the vol. and book but that doesn’t matter

Very helpful information. Thank you. My issue is the “Trust” to which my mortgage was assigned does not exist when I do the search. Its U.S. ROF III Legal Title Trust 2015-1 Any ideas??

This doesn’t tell you very much: http://www.sec.gov/Archives/edgar/data/1641795/0000897204-15-000064-index.htm

but it is filed in the SEC. Here is a contact at US Bank if she is still there: https://trustinvestorreporting.usbank.com/TIR/public/deals/detail/76644/us-rof-iii-reo-2015-1-llc-cash-account

All of this is great in theory but when the judgement has already been entered you are not entitled to discovery in court. If you can’t have discovery you cannot bring up anything about standing, this is what I have encountered when I went to court five different times, and they still foreclosed and took my home. Does anyone have any suggestions besides having to go to the Appellate Division who is in bed with the rest of the judges in the court system, how can you bypass the court and go to the feds or have somebody look at these cases? I was told I lost all my legal rights and it’s too late to do anything, I’m still holding on to hope and fighting, and I refuse to leave until the sheriff physically removed me. There has got to be a way that somebody in authority will listen, my loan was defintinely securitized, and there were several violations, 47 in fact.

Give it time. We’re getting there. Yvanova is just one example. More to follow. We’ll be posting some interesting behind the securitization process documents shortly that establish the homeowners as third parties to the transaction.

I am not sure ultimately how helpful this is to anyone trying to win a case. But it is interesting, and it answers a lot of questions to go through the process. Before one spends countless hours on rabbit holes of detailed minutia, they would be well-served to consult a lawyer to at least focus their efforts.

Absolutely contact a competent attorney. However, never stop investigating and educating yourself because no attorney knows everything as it changes constantly with new cases. A good attorney will be grateful for additional research. Now, as for how important it is to research the securitized trusts – every homeowner should try to locator their trust. Read the PSA, familiarize yourself with the process that is outlined. There are too many points to adequately define in just a short reply – but I can personally tell you of one homeowner who dissected all of his documents and has great comprehension skills that has helped his attorney immensely. His family is still in their home since 2009 and finally his judge is realizing the securitized trustee hasn’t been able to establish an unbroken chain of title.

This homeowner has also been able to establish that the homeowners are parties to the securitized trust documents. So, rabbit hole – yes…but Alice, you’ll find more than the Mad Hatter down there.

Oh, and BTW – if you find your trust verify your collateral is still actively trading. We have an Ocwen case where Ocwen has stated (in writing) that “the rating agency determined the amount of modification for the trust and that the trust had met its limit” (denying the modification) – however, using Bloomberg Terminal the homeowner was able to show that the trust was modifying loans every month… Major misrepresentation by Ocwen.

This maybe a bit lengthy! I need some direction on how to locate my PSA or even if I’m looking in the right place or with the right date or company. Closed on a house in Arkansas 6/28/07, however the documents filed with the county have the copy of my “note”, and MERS and Fannie Mae’s website saying 6-26-07. How could I have a mortgage note dated two days prior to when I closed on it with the title company? Also at the bottom of my mortgage documents I signed are numbers in the bottom right corner and the bottom left (I have realized one was my account number with USAA that I would have and the other is my account number with GMAC that I would have in 2012…how did I have an account number with GMAC the day I signed my mortgage with USAA and 5 years prior to my loan being tranferred to GMAC?). I assumed I originally bought the house through USAA Federal Savings Bank and made payments via their website. March 2012, I receive an assignment of mortgage claiming my loan had been transferred by MERS acting as nominee for USAA bank over to GMAC (also was a stamped name, Dannette Lowe who had “assistant secretary” stamped under her name and an allonge that was more of a second page rather than properly attached). GMAC starts a foreclosure in April and the house was to be sold at auction May 7th, 2012. I tried to do a short sale, which I supposedly was approved for by GMAC that never happened, and I tried to do a deed in lieu which was also denied. USAA said I didn’t have enough time to qualify for the loan modification options before my house was sold, so I decided my only option was to file for bankruptcy which prolonged my foreclosure some. In June 2012, I received info from GMAC saying they were doing a restructuring. In August I had been discharged from my Chapter 7 and did not reaffirm the house but had received a letter that GMAC and a bunch of other banks were declaring bankruptcy and this would halt any foreclosure attempts on me until they got through it. We were to stay put and await further instructions. GMAC never sent any more communication again and I kept living here.

Two years later in sept 2014, was the first time I heard anything about the house, which came in the form of a notice of auction by a company called Green Tree. I had no idea who they were and was completely surprised why they were trying to foreclose on me or how they had the right, so I hired a lawdid the usual foreclosure stall tactics which temporarily stopped the sale before Green Tree tried again a month later, this time sending “proof” of ownership in copies of my mortgage info including a copy of my note with red stamps of “True and correct copy” on every page.They gave the ALLY bank address in Iowa for the address of where my note was being held. Also in this packet of info was an assignment of mortgage from GMAC to Green Tree dated July 2014 with signatures by VICE PRESIDENT AND ATTORNEY IN FACT, Daniel Thompson and notary Nicole Baldwin (robosigners (Vice President of what exactly?). Sidenote…how did GMAC still function as a company in July of 2014 to assign my mortgage to anyone…weren’t they ALLY bank or OCWEN? By may 2015, I had dealt with Green Tree enough to know they were frauds and I started a lawsuit against Green Tree and GMAC with proof my assignment of mortgage was made of forged signatures that were identical to other people’s assignment of mortgages with other banks. GMAC managed to dodge all discovery questions in our court case and motioned for the judge to allow them off the case pending their ongoing bankruptcy (again, didn’t GMAC get sold in 2012? and their bankruptcy end in 2013?). The local judge closed the court case until GMAC could get their bankruptcy stuff figured out and we could reopen the case. Instead, Ditech shows up and goes behind the judges back and puts my house up for auction (Arkansas is a non judicial state) attempting to bypass court and steal my home. I hire my lawyer again and stop the sale of the house and sue GMAC, Green Tree and Ditech which is where we are currently.

I need help finding my PSA I think. Athough, I have read other sites that mention even having a PSA won’t help you. Since I have two mortgage dates, what does that mean and how do I know which date to use on the SEC website. I have also had problems as GMAC is missing a lot of dates around when I bought my house, and my loan might be under one of their other names. I think it is probably a Residental Captial, LLC loan more than likely. Fannie Mae also showed up around the time Green Tree did with an account number of their own for me and listing themselves as the owner of my mortgage (and Investor). Where did they come from and does this complicate me finding my PSA on the SEC website? Any advice on how to fight this whole thing in a state that has given MERS the right to foreclose on people is also helpful. I’m at a loss here.

Thank you for this great Blog. In your Blog dated August 26, 2013, about the New York Trust Law, my question is: does the Act EPTL 7-2.4 still active?, Because I have been hearing that it is not a ‘good law’ any longer. I will truly appreciate your answer. and if you have any updated recent cases to support that it is still a ‘good law’

There are some similarities with post above (AB on July 17) and my situation. Assignment of mortgage GMAC Mortgage LLC to Green Tree dated 9/16/2013. Kristina Emmanuel Vice President for Green Tree LLC, as attorney in fact for GMAC LLC and employed by NTC of Florida. Notary: Nicole Baldwin. Then…Corrective Assignment of mortgage to add Mortgage Electronic Registration Systems Inc. to the lender for 2nd mortgage and CEMA. GMAC Mortgage LLC assigns to Green Tree Servicing LLC dated 7/30/2014 signed by Daniel Thompson, VP Greentree Servicing as attorney-in-fact. Notary: Nicole Baldwin.

Green Tree started foreclosure proceedings. They filed motion for an order of reference which was denied without prejudice for lack of standing. I have been in the process of short sale and shortsale attny wanted to proceed with short sale after this. Mortgage was transferred by Fannie Mae to Goldman Sachs six weeks ago and servicer was transferred from Greentree to Rushmore loan servicing approx five weeks ago. My shortsale attorney is still asking for financials to send to Greetree/Fein Such and Crane (attny for Green tree) for shortsale approval after telling him they have no interest in this property anymore. Thoughts?

How can you do a short sale when there was lack of standing? They can never take the home fi they can’t prove ownership of note so why not keep fighting? If you sell home, are you gonna make money, is that why you want to do that? Won’t it be the crooked banks making the money?

Susan, I’m curious which state are you in? I have Ditech wanting to “settle” rather than go to court at the end of Oct. But they have also put in for the judge to dismiss my case because they are the “holder of the note”. The note which is incorrectly dated 2 days before I even closed on the house. It’s nice to know we aren’t the only ones!

Hi,

I live in the UK.

I believe the similar problems have occurred in the UK, with GMAC and Merrill Lynch. Is there anyway of finding out if your mortgage was part securitisation in the UK?

Thanks

No doubt it has occurred. I am checking with colleagues to provide you more information. Maybe UK courts will be more honorable… Think?

Can anyone help locate the list of loans bundled with MASTR Adjustable Rate Mortgages Trust 2007-1? I have read the FWP and the pooling and services agreement, as well as some if the initial filings, but only found loans listed under the default REO sections, and my default is beyond the last filing date since the trust was sued into oblivion.

When we are stumped we ask CFLA (Certified Forensic Loan Auditors) to do an “initial search” to see if the loan is actively trading in the trust. Many of the loans were sold to the Fed and if they can’t find your loan there then you might want a full search.

It would seem logical that if a loan is active in a trust (certificates are still trading) that the collateral is still part of the securities transaction until it is bought out from the trust. If that is the case, it appears that this is a non-traditional mortgage product and therefore, not a traditional mortgage. The argument many attorneys are wrestling with is how to argue this before the courts, because there are no laws for quasi-securities…but there should be.

If your attorney can convince the court that this was a securities transaction (and we know it was operating before you signed your documents) that securities law should apply. And until the loan is bought out of the trust, it is a non-negotiable instrument not applicable under UCC Article 3. So, if a trust has filed a complaint of foreclosure – it is worth exploring this avenue. This is theory – not legal advice. Discuss this with your attorney.

Pingback: How to Search the SEC for a Securitized Trust – boglinwordpresscom

Thank you for sharing this information. I think it will be very helpful to many of those fighting for their homes. Much appreciated!

Pingback: The Constitution of the United States, The Bill of Rights & All Amendments | Securitization | DEED OF TRUST & Mortgage Electronic Registration Systems [MERS] Et cetera – auggiecoupdblog

my loan is securitized it has been in a trust since 2000 it was simply put in a trust no trustee depositer etc they havent reported to sec for 15 years the note and the mortgage are irrevocably separated there is a record of an assignment to a different servicer the signature on this statement sa wileman president of centex corporation after investigating he is president of 5 different corporations all signatures same name appear differently when i checked further on my tila statement they understated my total finance charges by over 90000 dollars just wanted to know what your take is on this and what should i do with this information thank you bill werner

No REMIC trust I am aware of ever filed any report of payouts with the SEC after one year as they all claim to be exempt. They do not have to report anything and your issue is meaningless. The idea that the note and mortgage can be separated is pure nonsense thanks to the crap on the internet and people grasping at straws. The mortgage ALWAYS follows the Note. However, there are mortgage assignments that fail to assign the note and they are legally worthless and accomplish nothing. In other words, they do not create any standing.

So this is also an interesting one with our mortgage. Again, Bank of America took over CountryWide in June 2008, yet, nowhere on my SEC records is Bank of America listed. In fact, to this day, it still says CWALT which stands for Country Wide Alternative Loan Trust. The servicer even admits that the private investor is still CWALT, which is Country Wide.

CWALT, a special purpose entity, is the Depositor, and hence the name of the trust. It is NOT the investor nor is it the owner of anything. Also, it does not exist. Although Countrywide was merged into BofA, no documents are ever changed. Also in the case of a merger, no mortgage assignment or anything else is needed to demonstrate that.

So if I am understanding your comment correctly, the Loan Servicer, Specialized Loan Servicing, lied to me when they told me that CWALT was the private investor. That CWALT does not exist and that my loan then therefore does not exist. And since Country Wide is no longer, then Bank of America who turned my loan servicing over to SLS means that SLS has no claims either? As you can see this is very confusing to me and I am a fairly intelligent person.

This was found in the Lehman bankruptcy – issues still going on… I have the opinion is you want to research it for more info on how these SPVs worked. I’m beginning to believe that just like Lehman, none of these investment banks followed the Flow Agreements and that’s why US Bank as Trustee had to walk away from thousands of claims. See notes to Dan.

“The originator that creates and indirectly owns the trust owes no debt to the investors; rather, the trust is the legal owner of the pool of mortgages, known as the “collateral.” Each certificate entitles its holder to an agreed part of the cash flow from the mortgage loans in the collateral pool. See Fed. Home Loan Bank of San Francisco v. Deutsche Bank Sec., 2010 U.S. Dist. LEXIS 138564 (N.D. Cal. Dec. 20, 2010) (citations omitted).

Here, the MBS were packaged, “issued,” marketed, and sold by the Debtors through a securitization process in which LBHI assembled collections of mortgage loans for sale to investors (fn11) and then transferred the pooled mortgages to SASCO. Although the collections of pooled mortgages ultimately were deposited in non-debtor securitization trusts (the “Trusts”) by SASCO, because the Trusts were vehicles with no reporting obligations, employees, officers, or directors, they were referred to under federal securities rules and regulations only as “issuing entities.” See Objection at ¶¶ 9-10. The Trusts provided MBS certificates to SASCO, which served as the “depositor” for the MBS and, under the federal securities laws, also was considered the “issuer” of the MBS. (fn12) SASCO then sold the certificates to investors through underwriters. FN 12: The actual issuers, however, are the Trusts.”

It is meant to be confusing. Some of your issues though such as an “illegal loan” and the ADA are just a waste of space. There is no relief available under such arguments. Also, you said you are not being foreclosed, so this is not a pressing issue. Frankly, nobody here can give you legal advice or specific advice for your specific situation as you are not a client and the lawyers here do not represent you. I doubt anyone is going to research your specific situation for free. I have talked to a couple of people who are in a somewhat similar situation, their problem is that the ownership of the note/mortgage is so messed up they cannot sell their property. One thing I am certain of is that CWALT was the depositor and not an investor in the trust securities. If it was holding any securities, it would be in the first tranche which was paid off long ago and was the only tranche that was insured. Oh, want to hear a funny? I OWN the name CWALT, INC. in Florida and some other states. I own CWALT, Inc. in the county in which Bank of America is headquartered, just for fun.

Dan Schram, you crack me up with the ownership of the CWALT. I will look into some of this. And I do have an attorney who is interested in my case because it is so crazy. And yes, I am in an illegal loan that was banned in CT so that makes the loan illegal apparently and thus void.

What would be interesting discovery would be to ask for the Flow Agreement between the Originator, its entities, and the investment banks and their entities. Then ask for the executed documents between all the entities and their inter-company assignments to see if they match the Flow Agreement format. For example: “On February 22, 2017, the Honorable Coleen McMahon of United States District Court Southern District of New York affirmed that “U.S. Bank had “‘effectively abandoned’” and “‘walked away from’” hundreds of thousands of claims against the estate of Lehman Brothers Holdings for Lehman’s representation and warranty failures as RMBS Warrantors. Supplement. The bankruptcy claims abandoned by U.S. Bank concerned 60% of the one million mortgage loans that U.S. Bank initially claimed in 2009 as subject to repurchase.”

U.S. Bank, N.A. v Greenpoint Mortgage Funding, Inc. 2010 NY Slip Op 50371(U) [26 Misc 3d 1234(A)] Decided on March 3, 2010 Supreme Court, New York County Fried

“It is uncontested that (1) the Lehman entities did not use the form in question; (2) that the forms used were not substantially in the form of Ex. H; and (3) that neither the Lehman entities nor U.S. Bank obtained the loans, and the status of “Purchaser,” pursuant to any such form.”

“Plaintiffs’ argument is contrary to the plain language of the September 2005 Agreement and ignores longstanding New York law. The Lehman Holdings Assignment and the SASCO Assignment are not Securitization

Transfers under the September 2005 Agreement. That Agreement defines Securitization Transfers as transfers “to securitized trust structures.” (Id. § 28.) The assignment that ultimately transferred the Loans to the Trustee at the end of the assignment chain would meet the definition of a Securitization Transfer under the Agreement. But the Lehman Holdings Assignment (an assignment from Lehman Bank to Lehman Holdings) and the SASCO Assignment (an

assignment from Lehman Holdings to SASCO) do not meet this definition, because they are plainly not assignments “to securitized trust structures.” Instead, they are merely assignments from one non-securitized structure to another.”

“Under longstanding New York law, “an assignee never stands in any better position than his assignor.” Int’l Ribbon Mills, Ltd. v. Arjan Ribbons, Inc., 36 N.Y.2d 121, 325 N.E.2d 137, 365 N.Y.S.2d 808 (1975). Because the Lehman Holdings Assignment and the SASCO Assignment did not follow the required form, they could not convey Purchaser rights to Plaintiffs. The validity of the assignment chain was broken and cannot be repaired as a matter of law.”

Very Interesting idea. Whom do I ask for this stuff from? The Servicer or the Trustee or who?

The papers I have say Deutsche Bank Trust Company Americas formerly known as Banker’s Trust Company as trustee and custodian for Morgan Stanley Home Equity Loan Trust MSHEL 2007 – 2

the Loan was with Wilmington Finance Inc dated 12/18/2006 in CT Deutsche foreclosure with Ownew serviced the loan. I have looked and can not find the PSA any ideas!

Deadly Clear,

Can you please email me. I have 27 days(today is March 30) till a servicing company forecloses on the house my father left me and my 13yr old son. He passed away January 9th 2017, CHASE sold or transferred to Bayview Loan Servicing, LLC. I looked up the address in MERS and it brought up 5 different companies with INACTIVE and Dates of Note being old and only 2 on there I recognize but not with the correct dates of when they had the note. My dad had the mortgage originally from M&T, dated April 3rd 1998. Please help guide me, please. JLBulson@outlook.com

I have done ALOT of research and came across MERS on Tuesday then SEC on Wednesday.

I followed your steps from above and nothing pulls up, I have been trying different variations for 3 days now.

Please I’m a single mother, trying so hard to not just give up. I have been having ALOT of problems with BAYVIEW LOAN SERVICING, LLC since the “took over” the mortgage on October 5th 2017.

You need to contact a foreclosure attorney in your area. Post where you are located and we’ll see if we can help you find a knowledgeable foreclosure attorney.

Can u afford an attorney? That’s the best route. I have used a great one in Broward county Florida if you are in Florida. If you can’t find one right now, you can always try to answer the suit yourself. I am trying to get a copy of what a friend responded and you could use that. But again, an attorney is the best thing. Will be praying for you, Jennifer. With God, all things are possible and it’s a crime what these crooks are doing to you.

My friend has same bank trying again to foreclose. This time though, it’s a new trust that I read was bogus. I searched SEC and nothing comes up. It’s RMAC Trust Series 2016-CTT. There are lots of people having the same trust when their loan was many years ago. US Bank is the crooked bank trying to foreclose. They have been found not to even be a trustee for this trust but why can’t I find it on the SEC? Any help is appreciated. God bless.

Many defaulted loans (many billions of dollars worth) have been purchased by Lone Star Funding and sold into Master Participation Trusts, such as LSF9. These are Delaware Statutory Trusts. They are not registered or regulated by the SEC. Participation shares are sold only to institutional and qualified investors. If you see U.S. Bank Trust N.A. as the Trustee, this is what you are facing. This is a new beast but they are using the same fraudulent tactics as the REMIC trusts including bogus assignments, etc.

It is all so incestuous… but all in all it goes back to Fannie. “Lone Star Funds, which buys non-performing mortgages by the truckload from Fannie Mae and Freddie Mac and is the parent company of Caliber Home Loans…” see https://www.housingwire.com/articles/40818-lone-star-funds-shakeup-north-america-president-sam-loughlin-steps-down.

“Buys” is an interesting terminology. Betchya there are agreements under the agreements where Fannie still owns everything, no real money changes hands, and if “LSF” gets the homeowner out and a sale confirmation (which would likely be to Fannie or US Bank, etc.) that Fannie gets a large chunk of the deal or keeps the property for re-sale, re-securitization and rehypothecation. Fannie concealment. You never know who you are really dealing with, or if the original note still exists, who has it – if anybody. What a scam.

BTW – look for Calibur Home Loans on the Treasury TARP contract site, where Fannie is the “financial agent of the United States” https://www.treasury.gov/initiatives/financial-stability/TARP-Programs/housing/mha/Pages/contracts.aspx and you’ll find a couple more sleaze brothers under that umbrella.

You are correct, but so much is unknown. The trust agreement has never been produced in any case I have heard of. The Servicing contract does not have US Bank Trust NA as a named party, though they signed it for the trust vehicle. The first and last pages are on the web. I have seen the contract in other cases where a handful of paragraphs are provided on servicing followed by 50 pages of black squares. I have also seen different cover pages listing different parties. So it appears nobody in the foreclosure defense world knows any of the details of these trusts. It is my understanding that they pay 68 percent of face value for the notes/mortgages. That would have to be of the amount still owed I would think, which in most cases is probably less than the value of the property. They follow the REMIC model with fake assignments and move the note from the original lender directly to the trust which is legally impossible. It does not matter if it is a family trust, a REMIC or a Delaware Statutory Trust, ONLY the Depositor can put anything into the trust. They try to make them look like contracts but there is never any acceptance by the trust and contrary to the wording of the assignment, the Trustee or Trust NEVER EVER pay a single cent. The Depositor is the last party to actually pay anything. Then the Trustee issues the security certificates back to the Depositor for sale to investors. The original lender is never ever a party to any trust. The courts say the borrower is not a party, well hello, the original lender is not a party and the Servicer who is actually foreclosing is NEVER a party to the trust. The Servicer is also without standing and all the Powers of Attorney they use at trial (it the case gets that far) are fake and actually do not even accomplish what they claim.

I just found out that Bank of America sold my bank to a private investor who put me into some special loan program that prevents me from getting a proper loan modification. I was never told about any of this. What I was told that I had a new Loan Servicer, SLS and it then took me 2 more years to find out that Bank of NY Mellon was only a trustee. And it took me filing a federal lawsuit to find out about this program. Does anyone know what this program might be?

Long story shortened. 2008 Bank of America acquires Country Wide and thus my loan. They put me into a HAMP Loan Modification for 5 years that was only temporary and at the end of it put me back in the predatory loan that caused us problems. This is illegal under HAMP. In 2010, 2 years into the loan mod, I became legally disabled on a fixed income and notified Bank of America that the then present loan modification was all I could afford. They refused to turn my loan modification into a permanent. Flash forward to today. I have been through 13 loan modification attempts since then.

I filed a Federal Lawsuit against Bank of America, SLS, Bank of NY Melon, MERS and Wells Fargo. The judge dismissed 11 of my counts against them including the HAMP Violation and then removed all the defendants but the first two. In November 2017, SLS finally gave me a loan modification but refused to tell me the details of what the new loan modification would look like and what we would owe when the 3-month trial was over. In January, when the trial was over, they gave us a loan modification that was absurd.

Finally, my federal lawsuit was coming up and after 3 years, the judge finally assigned limited scope attorney who was ineffective. As soon as he met me with all of my evidence, he wanted off the case. But he agreed to stay on for mediation. During mediation, I found out that the Private Investor put my mortgage into some special program preventing me from getting an appropriate and proper loan modification. I had no knowledge of this program and I believe it was illegal as I was not notified, there was no consent by me and it was in direct competition with all of the loan modifications I had been in the process of trying for since 2013 when the original loan modification ended.

So again I ask, Does anyone know what this program might be? Or had an experience like this and have advise?

I was told by a former BOA manager that no money ever changed hands. In his words, “it’s all spreadsheets”. He helps homeowners to fight pro se and when I asked him why he changed ships, he responded that he knew they were trying to “buy him”. He shared how he went to a banquet for appreciation of bank managers and at the end of the dinner, they turned on the fans and began to throw out “thousands of hundred dollar bills”. He quit right after that. I asked if he was scared of the powers to be coming after him and he said that there were millions of these cases and that as long as he only helped those with small mortgages and not commercial real estate, that they would not bother with him. Yes it sounds like mafia. I had 2 attorneys tell me not to bother to help my friends fight the foreclosure and adamantly insisted to just modify because “you can’t win against them”. After I told one of them that my friend was willing to pay (I am her interpreter and know about all this stuff), he looked at me straight in the eyes and said in English (so she couldn’t understand), “I don’t want your money! Do you know who you are dealing with?!” Then he asked me if I knew of a certain inventor and what happened to him. I shrugged and said, “they must have blocked his invention”, to which his secretary interjected, “they killed him”. Then another time I was before an attorney who was mediating before the case could go to hearing and he couldn’t believe my friend refused modification deal where they would take off $220,000 off the principal. So I mentioned famous robo signer Linda Green and asked if he remembered what happened to her and he, too, looked at me square in the eyes and said with a smirk, “yeah……she’s dead!”

As for another part of the scam and heist of trillions of dollars, Chase Bank tried to foreclose and since they knew they couldn’t win, they went to HUD and got almost $200,000 on the property of my one friend. Then they substituted another party who couldn’t prove standing. They faked an assignment by HUD. Now another bank is trying to foreclose and HUD told me that if they fail, then they can submit insurance claim, too. So multiple banks can cash in on insurance, too, besides taking away the property. But the corruption is even bigger than just foreclosures.

This has got to stop!!! My girlfriend and i say the following:

No Government or Entity should be so powerful as to disrespect, ignore the laws, overpower and violate the rights of the people

You are absolutely right!!! I was born in Nicaragua and right now, the govt. has been using youth delinquents and police to kill at random. Yes it can get that bad if the good do nothing. Praying that you will find out about program and that you can find an attorney to take those who broke the law to court. Don’t stop fighting. My friend told me this morning that he is tired and wants to just let them have his house. But I almost yelled at him, exhorting him not to give up. These crooked banks and servicer have no right to get property they never paid for.

We need to find an attorney who is not afraid of the system or these crooks and is willing to start to file things as class action or something. We need a Watergate type investigation with news reporters possibly. This stuff has to stop before our country is entirely annihilated by this corruption. When is enough enough?

So many I know and work with have been retaliated against for speaking up and speaking out. This is not what our country was founded upon.

Dear Dan, the last time U.S. Bank tried to foreclose in 2015, this was the fraudulent transfer of hands:

1) Chase made fake assignment to HUD dated 2014 – LVS Title Trust 1.

2) Chase prepared fake assignment from HUD to US Bank (and HUD told us they don’t make assignments) – LVS Title Trust 1.

3) During the case, which they lost to my friend, another fake assignment from US Bank to UMB Bank – Mart Legal Title Trust 2015 – NPL1

4) Now 3 years later, fake assignment dated 2016, UMB Bank to US Bank is submitted with new foreclosure complaint – RMAC Trust, Series 2016-CTT

So how can the trusts be made into new trusts? Can you explain and how if it’s illegal, can this be brought to judge? God bless, S

Yes,i would like to know this too because I suspect that the trust company assigned by the private investor is also not legal.

Need to make a correction on why comment. It should have said, I just found out that Bank of America sold my loan/mortgage to a private investor who put me into some private program that no one can tell me anything about,

My friends are blessed with an attorney in Florida who is fighting again for them. He won the last times. One with the bank’s witness admitting he didn’t bring records from bank but got them from the bank’s lawyer and the second case cuz the bank couldn’t come up with documents. But both banks are back again after years trying again. There have been class action suits and all the banksters got was a slap on the hand. I want to bring this before the grand jury but I don’t live in the county where this happened. What’s hard is seeing how many don’t want to know what’s been happening because it hasn’t happened to them. I don’t even own a house. I live with my mother but I have to get involved cuz it’s criminal to see these banksters get away with stealing and killing. The mob got into real estate and banking.

Thank you for what you do, do. I work 24/7 with victims of abuse, in particular, Psychological abuse called Parental Alienation. I know what it means to these clients to have someone help them for free.

God bless you for what you do, too. The only way these cases go the right way, I have found, is thru intervention by the Lord. Even the attorney we have used doesn’t know everything about all this crookedness. He is having his eyes opened, though.

Yes, when I started in the work I do, most attorneys had no clue. I had to train and educate my husband’s attorney. I do not ask for much but fairness and that just does not seem to be how our courts are run anymore.

I always wondered how securitized looks like Mr. Deadly clear! Thank you!

Can u put me on your list if u planing on filing class action! Against criminal @WellsFargo betrayed us threw us babyboomer on st. Due to Fake modification

Help! My assignment says Westvue NLP Trust- I can’t find it in the SEC.

Search Westvue NLP Trust and Fannie Mae. Search Westvue Trust with US Bank. Search Westvue in the USTPO Trademarks (TESS). Many of these Trusts are private trusts and for some crazy reason don’t have to be reported to the SEC. Usually, Fannie is behind it. Paper laundering? Your discovery needs to be deep. Where are you located?