Nothing is more depressing than a state court judge that obviously favors the bank’s attorneys – even when the evidence clearly says the trust bank claiming to hold the documents is not the real party in interest. How could a securitized trust not have to follow the UCC securities code, Articles 7-9?

Nothing is more depressing than a state court judge that obviously favors the bank’s attorneys – even when the evidence clearly says the trust bank claiming to hold the documents is not the real party in interest. How could a securitized trust not have to follow the UCC securities code, Articles 7-9?

How could an actively trading trust with certificates issues against a static financial asset become a “Holder” under UCC Article 3 when the financial instrument is supposed to be non-negotiable until it is purchased at face value from the trust (to pay off the certificate holders)?

Personally, every case that gets reviewed and every transcript that is read where the Assignment of Mortgages are plainly fabricated and the judge turns a blind eye when he knows the bank attorneys are defrauding the court, just smacks of judicial corruption. And in America – this is very, very sad.

Over a year ago, Molly Rose Goodman, a JD Candidate, Suffolk University Law School,

Over a year ago, Molly Rose Goodman, a JD Candidate, Suffolk University Law School,

wrote The Buck Stops Here: Toxic Titles and Title Insurance and a year later state courts are still condoning the frauds. It’s not clear whether Molly even knew there are patents filed in the United States Patent and Trademark Office and World Intellectual Patent Office for all these bad acts – as if to legitimize the criminal behavior; but, why in these government bank settlements and fines, if they are not going to send the bad bank dudes to jail, aren’t they confiscating the patents that control and run this corrupt scheme?!

Ms. Goodman correctly writes, “Document fraud and robosigning became commonly

recognized phrases after the financial market collapsed in 2007. The rapid increase in foreclosure filings exposed documentation errors and deception that was commonplace

in securitization and real estate transactions throughout the housing boom. The continuous appreciation of property values and the success of securitization diverted attention from the industry’s systemic failure to comply with longstanding principles of property law.

Okay – that is a given. Every American homeowner and un-corrupt foreclosure judge should completely understand and agree that Ms. Goodman’s statement is true. This isn’t supposition – this is fact.

Okay – that is a given. Every American homeowner and un-corrupt foreclosure judge should completely understand and agree that Ms. Goodman’s statement is true. This isn’t supposition – this is fact.

Yet we still hear idiot judges whimper without due process of law, “You owe somebody… you’re not going to get a free house in my court” .

That used to be an acceptable philosophy 6 years ago and for the most part homeowners just needed and wanted a simple modification until they could reinvent themselves and get back on their feet after the 2008 crash. Well, as we learned later – the HAMP program was a pre-meditated scam designed to drive homeowners into default and then foreclosure. See Neil Barofsky’s BAILOUT, Chapter 8 – Foaming the Runway. As the years have passed and the securitization scheme was dissected for the criminal process that it is – homeowners, attorneys and honest courts began to see the cleverly crafted process for what it was (and remains) – corruption.

Since the turn of the last century (2000 – and before) fabricated fraudulent documents abound and were intentionally filed throughout the United States land records offices. And when cases that get too close to what really transpired – the courts push settlements, modifications with the wrongful parties rather then let a jury trial decide the fate of the banks. Why do you think that is?

Some judges (and attorneys) actually think that this securitization scheme is a physical paper-intensive process. That documents exist in file cabinets and cardboard file boxes with millions of physical documents stacking up all over the place and warehouses full of original loan information that got physically transported back and forth. Golly gee – how do we drag these draconian creatures into the 21st Century cloud computing where all the personal data is stored and is made VERY accessible to far too many people?! “Physical documents” and “physically transferred” are essentially an archaic state of mind.

Some judges (and attorneys) actually think that this securitization scheme is a physical paper-intensive process. That documents exist in file cabinets and cardboard file boxes with millions of physical documents stacking up all over the place and warehouses full of original loan information that got physically transported back and forth. Golly gee – how do we drag these draconian creatures into the 21st Century cloud computing where all the personal data is stored and is made VERY accessible to far too many people?! “Physical documents” and “physically transferred” are essentially an archaic state of mind.

Sara Angeles, staff writer for BusinessNewsDaily wrote, “2014, cloud computing is expected to become a $150 billion industry. And for good reason — whether users are on a desktop computer or mobile device, the cloud provides instant access to data anytime, anywhere there is an Internet connection.

For businesses, cloud computing also offers myriad benefits, such as scalable storage for files, applications and other types of data; improved collaboration regardless of team members’ locations; and saved time and money by eliminating the need to build a costly data center and hire an IT team to manage it.

For businesses, cloud computing also offers myriad benefits, such as scalable storage for files, applications and other types of data; improved collaboration regardless of team members’ locations; and saved time and money by eliminating the need to build a costly data center and hire an IT team to manage it.

Most businesses, however, have one major concern when it comes to cloud computing: Exactly how safe is the cloud? Although most reputable cloud providers have top-of-the-line security to protect users’ data, experts say there is no such thing as a completely safe cloud system.” Read more HERE.

This is how the banks share your information. Privacy? Nah – its been long gone since that first mortgage loan application. And this industry grew so fast without sufficient regard for the safety of the information – alas, Jamie Dimon is whining because his and other banks have been hacked.

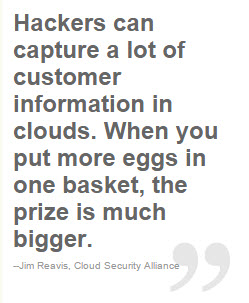

DigitalBiz did a story in 2010: “”We are very concerned about the bad guys using the cloud,” said Reavis. “[Hackers] have the ability to move laterally and capture a lot of customer information. When you put more eggs in one basket, the prize is much bigger.”

DigitalBiz did a story in 2010: “”We are very concerned about the bad guys using the cloud,” said Reavis. “[Hackers] have the ability to move laterally and capture a lot of customer information. When you put more eggs in one basket, the prize is much bigger.”

Bad guys also have the ability to infect clouds with spyware, botnets and other malicious programs, Reavis said.

In January, Google announced its web-based Gmail system had been compromised by a malware attack originating in China. As a result of the breach, Google announced it would stop censoring its Google.cn search engine and possibly end business operations in the country.

“We expect a whole new generation of malware to come out of things that are specifically designed for cloud providers,” said Reavis. “We can imagine some very sophisticated next-generation hyper botnets that are very hard to defend against.”

A final concern surrounds privacy.

In the United States, where many cloud companies are based, legal standards make it much easier for law enforcement to obtain data for criminal or other investigations, said Kevin Bankston, a senior staff attorney with the Electronic Frontier Foundation, a San Francisco-based digital rights group.

“Data stored in the cloud is substantially easier for the government to obtain than the data you store yourself because of lower legal standards,” Bankston said. “And it is easier to do it secretly. We think this is a serious security concern, and the law needs to be updated.”” Read more HERE.

The point here is that your personal information, your documents, your history and hobbies are floating in this new cloud technology. Your originals got whisked away, without your permission (guess the banks felt it was better to ask forgiveness rather than permission) and it all happened so fast that neither your local or federal politicians, nor the judiciary could grasp the phenomenal effect it was going to have on the lives of everyday citizens.

This “cloud” technology is not a fluffy, puffy, white marshmallow system – its software (patents) provide for alteration and manipulation… just like that wonderful Wells Fargo Manual on how to craft fraudulent foreclosure documents and its patent software program VendorScape. The information is accessed and manipulated in cyberspace – it didn’t come from some manila folder in a file cabinet that had been there for years. It was created especially to scam the courts and homeowners – when will the courts wake up?!

This “cloud” technology is not a fluffy, puffy, white marshmallow system – its software (patents) provide for alteration and manipulation… just like that wonderful Wells Fargo Manual on how to craft fraudulent foreclosure documents and its patent software program VendorScape. The information is accessed and manipulated in cyberspace – it didn’t come from some manila folder in a file cabinet that had been there for years. It was created especially to scam the courts and homeowners – when will the courts wake up?!

More cases are proving that mortgage companies like New Century sold their loans simultaneously to investment banks – not to the actual securitized trusts. And whatever the investment bank did with the homeowners’ collateral and credit is in many cases is an all out mystery. One theory is that when the asset reached the investment banks it was sold numerous times in various swaps, CDOs, hedged bets, etc. over and over like The Producers and that’s how Wall Street got $700 TRILLION in debt. Of course, Wall Street wouldn’t want to record an assignment because the other investors would know the asset had already been sold… or maybe it would just make it easier for the courts to figure it out.

In any case, documents alleging assignments or transactions by a non-entity like America’s Wholesale Lender or a bankrupt entity, for example, New Century Mortgage Corporation years after the liquidating bankruptcy had been filed – and made without a court order… and after the New Century bankruptcy court has said that the asset was never part of the estate – are just plain fictitious. This isn’t so hard to see – unless, of course, the court is just a collection agency for the crooks.

In any case, documents alleging assignments or transactions by a non-entity like America’s Wholesale Lender or a bankrupt entity, for example, New Century Mortgage Corporation years after the liquidating bankruptcy had been filed – and made without a court order… and after the New Century bankruptcy court has said that the asset was never part of the estate – are just plain fictitious. This isn’t so hard to see – unless, of course, the court is just a collection agency for the crooks.