A landmark decision was made this week in Culhane v. Aurora in the United States Court of Appeals For the First Circuit without a complete set of facts set out before what appears to be its clueless judges.

A landmark decision was made this week in Culhane v. Aurora in the United States Court of Appeals For the First Circuit without a complete set of facts set out before what appears to be its clueless judges.

The case decision, an APPEAL FROM THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF MASSACHUSETTS was to some degree based on the merits of standing answering the question: “Whether a mortgagor has standing to challenge the assignment of her mortgage — an assignment to which she is not a party and of which she is not a third-party beneficiary — is a matter of first impression for this court.”

While the Court held: “We conclude that a nonparty mortgagor, like the plaintiff, has standing to raise certain challenges to the assignment of her mortgage,” it then turned to the “Validity of the Assignment” and did so under the false impression that the entity they assumed to be the major player – was indeed just a straw man; an asset-less shell without employees and certainly no members.

“The plaintiff’s claim hinges on the asseveration that MERS did not legitimately hold the mortgage at the time of assignment and, therefore, had nothing to assign to Aurora. [. . .] Here, moreover, MERS had the authority twice over to assign the mortgage to Aurora.” ?? Um, maybe NOT…..

Chief Judge Sandra Lynch, Judge Souter and Judge Selya apparently didn’t have all the facts in front of them in this case. But by now, if they are reading any of the foreclosure blogs, they’d certainly find the MERS issues suspect – to say the least. And wouldn’t ya think by the time the parties got up to the United States Court of Appeals, the clerks would have pulled every record and file on Mortgage Electronic Registration Systems, Inc. (all 3 of them) that they could find that pertained to its authentic existence before allowing their bosses to render a decision?

Chief Judge Sandra Lynch, Judge Souter and Judge Selya apparently didn’t have all the facts in front of them in this case. But by now, if they are reading any of the foreclosure blogs, they’d certainly find the MERS issues suspect – to say the least. And wouldn’t ya think by the time the parties got up to the United States Court of Appeals, the clerks would have pulled every record and file on Mortgage Electronic Registration Systems, Inc. (all 3 of them) that they could find that pertained to its authentic existence before allowing their bosses to render a decision?

Granted the securitization Ponzi scheme is intentionally convoluted, fraught with fraud and the road is paved with corruption, but the decision the 3 judges of the United States Court of Appeals For the First Circuit rendered may be in error because, honey – “the old gray mare, she ain’t what she used to be, ain’t what she used to be, ain’t what she used to be. The old gray mare, she ain’t what she used to be, many long years ago.” No, MERS ain’t what she used to be…

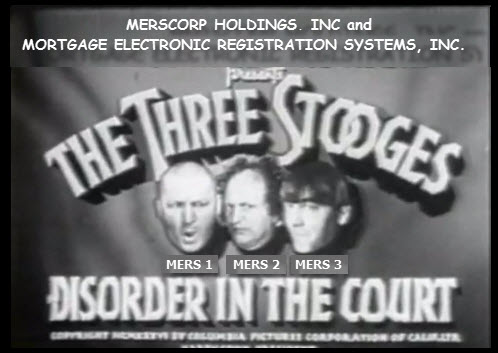

It’s hard to tell if this information might have made a difference – but there were 3 Mortgage Electronic Registration Systems, Inc. formed over the years. The trademark “MERS” was absorbed by MERSCORP, Inc. in the name change of MERS (II) in 1999.

It’s hard to tell if this information might have made a difference – but there were 3 Mortgage Electronic Registration Systems, Inc. formed over the years. The trademark “MERS” was absorbed by MERSCORP, Inc. in the name change of MERS (II) in 1999.

These documents are posted on the blog sites: www.deadlyclear.com and www.doctelportal.com (in its Library). There were 3 separate and distinct MERS entities. These are individual corporations. MERS 1 and 2 are gone – eaten up by MERSCORP, INC. The MERS 3 corporation in the mortgages in merely an acronym, straw man, no assets, no employees no members – just a shell and the courts have never been challenged with determining the difference. It appears that the court in Landmark might have understood this – but not many attorneys have taken the time to research the MERS vs. MERS®.

LANDMARK v. KESLER: The relationship that MERS has to Sovereign is more akin to that of a straw man than to a party possessing all the rights given a buyer…[. . .] What meaning is this court to attach to MERS’s designation as nominee for Millennia? The parties appear to have defined the word in much the same way that the blind men of Indian legend described an elephant–their description depended on which part they were touching at any given time.

In a Hawaii case, during limited discovery American Savings Bank (ASB) admitted that they were members of MERSCORP, Inc – NOT Mortgage Electronic Registration Systems, Inc. and discovery like this could be a game changer.

Court decisions are only as good as the material set forth before the judge. If the court hasn’t been asked to clarify the difference or determine the definition – it will likely avoid the conflict. Unfortunately, every rock has to be uncovered and every skirt lifted to find out how these guys rigged the system …and, as we all know too well, discovery is very hard to get to – that needs to change in order to obtain justice.

If the fact that MERS is not the membership party; and, MERSCORP, INC. is the actual entity and who did not contract with the homeowners – then let’s look at these issues within the Justices’ Decision after they have defined MERS as Mortgage Electronic Registration Systems, Inc.:

If the fact that MERS is not the membership party; and, MERSCORP, INC. is the actual entity and who did not contract with the homeowners – then let’s look at these issues within the Justices’ Decision after they have defined MERS as Mortgage Electronic Registration Systems, Inc.:

“Various entities involved in the residential mortgage lending business can become “members” of MERS. As such, they pay an annual fee and agree to the rules of membership. Lender members may name MERS as mortgagee in mortgages that they originate, service, or own.”

Nope – NOT true. The membership is not with “MERS the acronym” of Mortgage Electronic Registration Systems, Inc. The membership is with MERSCORP, INC., a separate corporation as of 1999, who did not contract with the borrower. MERS in the mortgages as of 1999 is merely a trade name, strawman – shell entity.

“Various entities involved in the residential mortgage lending business can become “members” of MERS. As such, they pay an annual fee and agree to the rules of membership. Lender members may name MERS as mortgagee in mortgages that they originate, service, or own. [. . .] There is one condition: the party for whom MERS serves as nominee must be a member of MERS. The upshot of this arrangement is that MERS holds the legal title to the mortgage as mortgagee of record, but it does not have any beneficial interest in the loan.”

Nope – NOT true. Again, the membership is with MERSCORP, INC. – not Mortgage Electronic Registration Systems, Inc. The members would use and belong to the MERSCORP, INC. system – MERS®, not the acronym.

“If a note within the MERS system is sold to a nonmember, MERS assigns the mortgage to the new noteholder or its designee.”

“If a note within the MERS system is sold to a nonmember, MERS assigns the mortgage to the new noteholder or its designee.”

Nope – NOT true. There is a distinct difference between the the MERSCORP, INC’s MERS® system and MERS the acronym. MERSCORP, Inc. absorbed the 2nd (of 3 companies named the same); and it was the 2nd Mortgage Electronic Registration Systems, Inc. that owned the trademark which was then applied to the system within MERSCORP, INC. – NOT Mortgage Electronic Registration Systems, Inc. in the mortgages. MERS® makes the assignments and tracks the loan – not the acronym strawman MERS.

“To expedite the execution of assignments, MERS designates “certifying officers.” These “certifying officers” are typically employees of member firms. MERS authorizes these persons, through formal corporate resolutions, to execute assignments on its behalf.”

MERS does not designate certifying officers; MERS® the system owned by MERSCORP, INC. does the certification within its membership guidelines.

“After making the loan, Preferred (a MERS member)…”

Nope – NOT true. Preferred is an member of the MERSCORP, INC. system MERS® – NOT MERS the acronym. Mortgage Electronic Registration Systems, Inc. has no members.

“In an assignment dated April 7, 2009, MERS transferred the mortgage to Aurora.”

The question here is can a straw man, trade name entity contract? It owns nothing, has no employees. It does not keep the records. It does not own the system – it does virtually nothing but appear in the mortgages as a fake nominee.

“We reject this thesis: there is no reason to doubt the legitimacy of the common arrangement whereby MERS holds bare legal title as mortgagee of record and the noteholder alone enjoys the beneficial interest in the loan. ‘

The question here is can a straw man, trade name entity, with no assets , no employees hold bare legal title?

“Thus, MERS’s role as mortgagee of 7 record and custodian of the bare legal interest as nominee for the member-noteholder, and the member-noteholder’s role as owner of the beneficial interest in the loan, fit comfortably with each other and fit comfortably within the structure of Massachusetts mortgage law.”

Nope – NOT true. MERS held nothing because MERS, the acronym was a shell. The MERS® system held and tracked the notes and it was under MERSCORP, Inc. by 1999.

“In the assignment, MERS transferred to Aurora what it held: bare legal title to the mortgaged property.”

“In the assignment, MERS transferred to Aurora what it held: bare legal title to the mortgaged property.”

Nope – NOT true. By 2006 when this loan was originally written – the MERS® system had long been absorbed into MERSCORP, INC. In fact it was actually a name change of the Mortgage Electronic Registration Systems, Inc. (II) to MERSCORP, INC. and the newly formed MERS (III) occurred shortly after the name change. So, why didn’t they change the name in the mortgages? Probably because confusion is the better part of valor…?

“While MERS’s practice of appointing employees of member firms as certifying officers can be disparaged on policy grounds, such policy judgments are for the legislature, not the courts.”

Nope – NOT true. It was not MERS’ practice – it was MERSCORP, INC. a separate entity that certified the officers.

“This is all basic, bedrock, foundational law, MERS cannot sign documents as there is no MERS, anything they signed and filed is without foundation and is manufactured to wreak a deception upon the Court to gain advantage to which the entity is not entitled to, and under the equitable principles of Keystone Driller, 290 US 240, at 245, the doors to the court house are to be shut in limine, their cause cannot be heard, and they shall gain nothing.” (Thanks again, Jan)

Was Mortgage Electronic Registration Systems, Inc. a legal entity or just a trade name? If it was merely a strawman covering for the “real” MERS® how can it assign or become a mortgagee?

it was merely a strawman covering for the “real” MERS® how can it assign or become a mortgagee?

Courts have distinguished the roles of trade names, for example AMERICA WHOLESALE LENDER v. PAGANO stating,“We conclude that, because a trade name is not an entity with legal capacity to sue, the corporation has no standing to litigate the merits of the case.”

AMERICA WHOLESALE LENDER v. SILBERSTEIN also found;

“An assignee, however, may not commence an action solely in a trade name either, regardless of the entity to which the trade name applies, because a trade name is not an entity with the legal capacity to sue. Nor could Countrywide cure the jurisdictional defect by substituting a party with the legal capacity to sue on behalf of the trade name. The named plaintiff in the original complaint never existed. As a result, there was no legally recognized entity for which there could be a substitute.” [. . .]

...and continues

[. . .] Furthermore, because America’s had no standing to bring an action, no action in this case ever was commenced, as it was void ab initio. In the absence of standing on the part of the plaintiff, the court has no jurisdiction.

No, MERS ain’t what she used to be…

Now, the final thoughts deal with how would these mortgage-backed securities decisions affect the Wall Street investments of the judges that over see them. Chief Justice Lynch probably should have considered recusing herself – her financial disclosure statement portfolios have been loaded with bank and Wall Street stocks and mutual funds. The same could be said for Judge Selya whose financial disclosure statements indicate he too is heavily invested in Wall Street.

Decisions that go badly for MERS takes the helium out of the balloon – just like it would deflate the portfolios belonging to the judiciary.

Whether or not you are represented by an attorney understanding the legal system is an asset. The more you learn, the less likely you are to be taken advantage of or scammed. Knowledge is power!

http://www.massnews.com/2003_Editions/3_March/030703_mn_american_legal_system_corrupt.shtml

Excellent article!

Folks we need to stop using the term ‘entity’ so loosely – as well as ‘straw name’ – they are fictional nonexistent names only – a human is a ‘person’ and corporations are ‘people’ too. If a name in the K (contract) is fictional-non-existent it lacks capacity to both enter/bind a K – as well as has no capacity to sue either.

If the so-called “lender” never existed it never had capacity to enter/bind a K not only with borrower but also lacked capcity to enter/bind a K with MERSCORP, Inc. as a ‘member’ and never was associated with the acronym MERS as recited in the mortgage as it too is fictional nonexistent as recited.

Courts are very critical about not disrupting the K’s language – thus there should be absolute care taken to ensure the so-called principles and recited terms are all lawfully in existence or the entire integrity of the K collapses as void at origination ‘void ab initio’ – there is no other way to categorize or move forward – doc correction had to occur within K dispute SOL’s usually 4-5 years otherwise – 30 years later is way too late in the game for finding out the K was never legal or binding with a fictional name only.

Papergate, very interesting take on the issue of “entity” and “strawman”. Where would i go to find more in depth info about this. I am in the process of wrapping my head around the legal fictions on both sides of the fence, as well as the so called “collective entity” doctrine that the courts use as an adhesion contract with us (of course without our knowledge). I have been dealing with a top to bottom fraudulent mortgage/RMBS/servicing ordeal where the fraud is like an onion, just keep pealing and there is more, more more, .

IMHO someone first has to bring the facts before a court and have the determination made that these three corporations were separate companies. One corporation changed its name to MERSCORP,INC. and then the third was formed; however, it has no assets, no employees, no members. #3 is a shell. But I would think in order for #3 to be recognized as part of the MERS(r) system a corporate veil would need to be pierced and usually that only happens when there is fraud.

The borrower did not knowingly contract with Mortgage Electronic Registration Systems, Inc. Personally, at the signing of my own mortgage, I asked the loan officer who it was and she said she didn’t know for sure…but it sounded like a recordation service. If these slick banksters, including Fannie and Freddie, had used the correct corporation, MERSCORP, INC., people may have caught on sooner to the scam of separating the mortgage and note and selling the loans on Wall Street. I got out of the stock market after ENRON – it was obvious how over leveraged and manipulated these companies are and I foolishly thought real estate was safer. We’d of all had more fun blowing the money in Las Vegas – it’s about the same thing – probably with better odds.

Reblogged this on Justice League.

IMHO its contract law 101 – attack the basic 4 corners of the K – it’s like a marriage – you need to know who in the hells sleeping next to you for 30 years – it is a lifelong K – it needs to be airtight to survive – to keep the integrity intact – I demanded they CORRECT the K in ’08 they ignored it – actually they were clueless had no idea what I was talking about – cause I was talking to entry level ‘customer service’ reps who knew diddly about what was going on. The point is this, we are all entitled by basic fundamental black letter law to be in a lawfully entered and binding K to protect both lender and borrower – why? Because at the end when you make that final last ah ha payment – you expect to be able to get your property cleared of all encumbrances or at least your heirs (kids) but you will not get that because you were never ‘sleeping’ with a ‘person’ who was ever legally existing and capable of being in a K with you – that’s why – so you made all those payments all those years to end up with not a single person, court or any forum able to assist you because you never had a valid real party that was legally existing and capable of entering into a K with you or MERSCORP, Inc. So there is no one or thing that will be able to re-convey your rights to you in the end – that is where the real wars and pandemonium will begin when millions of people begin to pay off on Ks that were never valid because no one was legally binding them – and there will need to be major, major conduct by government, legislature, whatever to handle the tsunami of cases of homeowners not able to get their re-conveyances and forget about getting the original note back- that’s an absolute joke – if those in charge don’t want to hear the arguments before us here and now – well perhaps they need to take a second look at the entire scenario from the perspective of what will happen in 30 years when no one is around – to indemnify or assist the homeowner – that is where and when the real problems are going to occur. People need to determine here and now exactly who it is they are ‘yoked’ with – married to in essence – check out secretary of state websites for each state – if the EXACT manner is not coming up – and don’t add on things like Inc., LLC on your own if they are not in the description – search the lender named exactly as it appears with your state’s secretary of state – it you don’t find that exact wording – you’re sleeping with a corpse that ain’t going away without litigation.

And remember, if that named lender is a corpse – fictional non-existing – then it will never have been able to be a valid or lawful member of anything – much less a database system because it does not have a ‘corporeal’ existence in which to know what an offer is; be able to accept something it has no way of comprehending; and certainly since it doesn’t exist on paper it will not have a ‘bank account’ or any other means of receiving monies or payments – or “consideration” which needs to be part of a K – it is a 2 way street that has only been a 1 way – 1 principle (homeowner) – in contract privity with itself – that does not make a valid K – it takes at least 2 ‘people’ to be able to agree and bargain for a K – if you are named alone with a fictional non-existent name – then there is no K – never was and never will be – that’s what you need to keep your fundamental argument and focus dead set on – because that it what is the underling ‘itch’ the thing that has been bugging us these past 4-5 years – something wasn’t right about our ‘transactional relationships involving our homes’ but we couldn’t put our fingers on what was stinking – this is it – so basic we have all been tripping over a tiny pebble – look to the K – also keep in mind aspects in this wonderful article about the 3 MERS – I argued that awhile back and everybody has shut up – not a peep from any enemies for 2 years – because they know they ar stuck and this is where we need to stick them – this is their Achille’s heel – it’s not the show me the note – combine the named lender and what has been stated in this article – the combination is lethal – fictional named lender and a straw name that is INCAPABLE of either entering or binding a K because it is incapacitated – it has no corporeal ability to engage in an offer/acceptance/consideration because there is no legal designated human for a database – now if they would have inserted the MERSCORP, Inc. with the MERS(r) that is a different story. But in these millions of cases, they failed to do that – they know it and now they know that we know it and we’re going to use it as a defense that a court cannot re-interpret the language of a K – it is forbidden – don’t believe me – go look at cases where the judge’s opionions state they cannot tamper with the K language it is not ambiguous – it is just simply in these cases – a miscarriage – a non-consummated yoking – think of it as a marriage – did you marry an assumed named body? Well annul that marriage right quick – same thing – these Ks were never consummated – they were never capable of being consummated never capable of being entered and legally bound for 30 years which is why there are no signatures or executions on these docs by anyone but the homeowner – it’s axiomatic – called plausible deniability – or something similar – it reminds me of when Hannibal Lector to Starling to “Look into your self’ it was so simple and stupid – double check your K – look inside the meanings of the words recited as ‘lender’ if what is there does not show up with secretary of state website name search – then you have a problem – call the party asserting putting them on notice you’re disputing the contract which a K dispute is 4-5 years – request that they CORRECT or REFORM it otherwise – it is trash and nothing more – worthless paper – file a notice of intent to sue for breach of K from gestational origination (before you signed) when they were crafting the note/mortgage – they knew what they were doing – they wanted to keep these notes/mortgages ‘untethered’ or stupid so no one would ask questions of the ‘lender’ – such as – do you mind if we steal your corporate asset without resolutions or minutes wherein corporate members agreed to sell or to something with IT’S asset meaning the K – they never wanted to modify correct or anything else because the truth would come out – they also used very cleverly worded ‘names’ to fool us into thinking we had a K with a genuine, non-fictional, existing entity, when we never did. We were duped so they could have merely MIN numbers to use as poker chips in a gaming parlor – at our expense and the joke is on the homeowner and the check – go ahead – pay the $300,000-$600,000 over the next few decades – and remember this article and commentary as we told you so.

Shelter, You hit it right on the head from ALL angles. We here in MASS run the Massachusetts Foreclosure Defense League. We are comprised of HIGHLY knowledgeable citizens and the few corrageaous, dedicated, and brilliant Atty’s who understand and litigate against the ” rot ” down to the core that you eloquently describe here. (Glenn Russell Esq., George Babcock Esq., et al. and the likes of Registrar John O’Brien (Essex County Registry of Deeds) – who had us down to his office where after our meeting he showed us what Mr. O’Brien’s office has called the “Crime Scene” – 35,000 Robo Signed documents on the tables.

Many of us were in the Fed. Court Room in Boston the day Culhane was heard and the 3 Stooge Judges were pretending to hear the case on its [true] merits. Get in touch with us. We could use your expertise. We sent a few of us to DC to educate the OIG’s office (at the offices explicite request). Keep writing the way you do. And regarding MERS, 30 year Atty. Robert M. Janes is writing a book as we speak on MERS; he calls them “Shell-Game MERS” and and you should shoot him a copy of your entry above. His first book “Fighting the ForeClosure Machine” is a good one.

In Peace..

John – Massachusetts Foreclosure Defense League

Third Circuit Case law bars such a claim. See Giles, 2012 WL 4506294, at 20 (Plaintiffs may not therefore, challenge any assignments to which they were not a partty” ) Ifert v. Miller, 138 B.R. 159, 163, 166 (E.D. Pa. 1992), aff’d 981 F.2d 1247 (3d Cir. 1992).

dockets.justia.com/docket/new-jersey/njdce/1:2012cv07910/283283/

Dec 28, 2012 … Plaintiff: FRANCES ROGERS. Defendants: BRAD A. MORRICE, GOLDMAN SACHS GROUP, INC., … Search for this case: ROGER v.

[PDF]

IN THE UNITED STATES DISTRICT COURT FOR …

docs.justia.com/cases/federal/district-courts/new-jersey/njdce/1:2012cv07…

Jan 28, 2013 … FRANCES ROGERS,. Plaintiffs, v. BRAD A. MORRICE, et al.,. Defendants. HON. JEROME B. SIMANDLE. Civil No. 12-7910 (JBS/KMW) …

April 24, 2013 at 8:10 PM

Pingback: MERS – TOO MANY DEAD DUCKS | Deadly Clear

Pingback: The Road to Securitization: MERS – TOO MANY DEAD DUCKS | My Debt Release news

Pingback: ShellGame-MERS: Contrived Confusion – A MUST READ! | Deadly Clear

Pingback: “Height of Hypocrisy” – Legalize MERS with a National Mortgage Data Repository aka Foreclosure Fraud-Away | Deadly Clear

Pingback: OCC – Correcting Foreclosure Practices | Deadly Clear

Pingback: TBTF HAS MET ITS WATERLOO | Deadly Clear

Pingback: THE HISTORY AND DEATH OF MORTGAGE ELECTRONIC REGISTRATION SYSTEMS, INC. ACCORDING TO THE USTPO | Deadly Clear

The CANCER of these CRIMINAL Scams is EXTREMELY EXTREMELY Widespread. It is Up To Us to UNIFY all the Groups and DECAPITATE the SNAKES ….. JBW https://www.bing.com/search?q=trillions+looted+toxic+zombie+land+swindles&FORM=HDRSC1

The Crime Scene is far far far LARGER than MERS ….. https://www.google.com/search?ei=AVuAW_DxM424tQXBppawAg&q=Mortgage+Fraud+Land++Fraud++Bank+Looting&oq=Mortgage+Fraud+Land++Fraud++Bank+Looting&gs_l=psy-ab.12…0.0.0.5587.0.0.0.0.0.0.0.0..0.0….0…1..64.psy-ab..0.0.0….0.RLkzAgubLz8